Tracking money coming in and going out

Corey Peterson

Corey Peterson

The habit that transforms your money forever

Think of tracking your money like checking your phone’s battery.

You don’t want it to hit 1% unexpectedly — and your money works the exact same way.

When you track what you earn and what you spend, you’re not being strict. You’re being aware. And awareness is what gives you control.

This module will teach you how to see your money clearly — where it shows up, where it disappears, and how to keep more of it working toward your goals.

Why Tracking Matters

Most people think they know where their money goes.

Most people are wrong.

Tracking your money does three big things:

1. Reveals hidden spending

The $7 snack.

The random $3 app purchase.

The extra $12 delivery fee.

These add up faster than you think.

2. Shows your real habits

Are you a saver?

A spender?

A little of both depending on the week?

Patterns matter — and tracking helps you see them.

**3. Gives you the power to adjust

before money gets tight**

No surprises.

No last-minute panic.

No “I swear I had $40” moments.

Tracking is the foundation of financial confidence.

Step 1: Know What Money Is Coming In

This is the easy part — list every way money enters your life.

Common examples:

- Allowance

- Chores or household tasks

- Part-time job

- Tutoring, babysitting, pet-sitting, yard work

- Holiday or birthday gifts

- Sports refereeing or coaching

- Freelance gigs (editing, art, reselling items, etc.)

You don’t need to track every penny forever — you just need to know your typical weekly or monthly income.

A simple chart works:

| Income Source | Amount | How Often |

|---|---|---|

| Allowance | $25 | Weekly |

| Babysitting | $40 | Every other week |

| Birthday money | $100 | Once a year |

Even having this written down makes your money suddenly feel more real.

Step 2: Track What Money Goes Out

This is where real transformation happens.

You don’t need to write down every single purchase forever — but you do need to track for at least 2–4 weeks to understand your patterns.

Spending categories to track:

- Snacks and food

- Clothes

- Entertainment

- Subscriptions (streaming, gaming, music)

- Transportation

- Gifts for friends/family

- Random purchases

- Savings contributions

Write them down the moment they happen or use your phone’s Notes app.

Here’s the secret:

Tracking isn’t about judgment — it’s about clarity.

If you see you spent $80 on snacks last month… congratulations. You discovered a money leak. That’s progress.

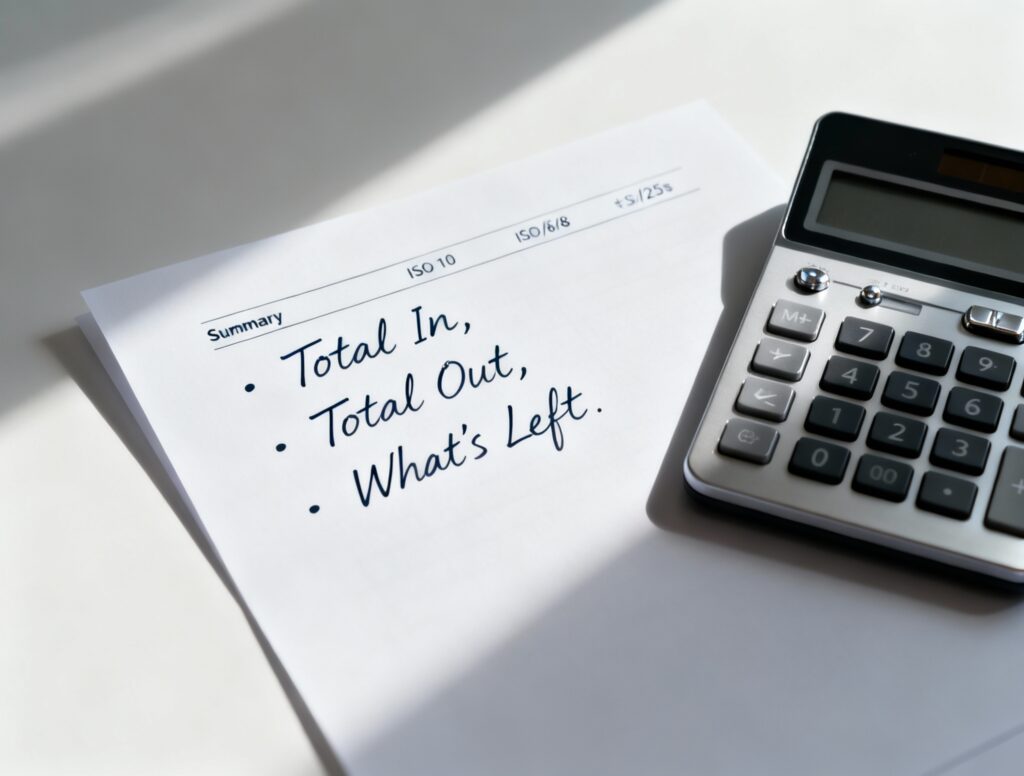

Step 3: Create a Quick Snapshot

After you track for a little while, write a simple summary:

Total Money In – Total Money Out = What’s Left

If the number is positive:

Great — you’re on your way to saving and planning.

If the number is zero:

You’re living right on the edge. Time to tighten things up.

If the number is negative:

Now you know why money feels tight — and you can fix it.

Awareness is the win.

Step 4: Use What You Learn to Build Better Habits

Tracking is only useful if you do something with the information.

Ask yourself:

- “Do I like where my money is going?”

- “What would I rather spend on instead?”

- “Are there small habits I can change?”

- “Is there a money leak I didn’t realize?”

Small adjustments lead to big results:

- Cutting one $6 drink a week = $312 a year

- Canceling a forgotten subscription = instant savings

- Packing snacks instead of buying = huge monthly differences

This is how financial independence starts — not with giant income, but with smart awareness.

Step 5: Make Tracking Easy (So You’ll Actually Do It)

Here are simple methods that actually work:

1. Phone notes app

One line per purchase. Surprisingly effective.

2. Budgeting apps

You can link an account or enter things manually.

3. Paper notebook

Old-school but powerful.

4. Screenshot your bank activity weekly

Then highlight your spending categories.

The right method is the one you’ll use consistently.